Exploring long-term care insurance (LTC) can seem challenging at first. Should you even buy coverage? If so, which policy type and company should you buy from?

And what about having to deal with some pushy insurance agent? That’s a lot of fun 🙁

There is NEVER any pressure or obligation with our service! We help you explore the best options available. If you change your mind anytime, simply tell us to close your file.

- What is Long-Term Care Insurance and Why You Might Need It

- Types of Long-Term Care Insurance Policies

- Is Long-Term Care Insurance Right for Me? Best Age to Buy LTC

- How Much Does Long-Term Care Insurance Cost (With Examples)

- What to Expect from Long-Term Care Insurance Underwriting

- Top Long-Term Care Insurance Companies in 2024

- Choosing Your LTC Policy

- Long-Term Care Insurance Tax Deductions: What You Need to Know

- Long-Term Care Insurance by State

- FAQ

- Final Thoughts

What is Long-Term Care Insurance and Why You Might Need It

Long-term care insurance (LTC) covers the expenses that your health insurance, Medicare, or supplemental insurance policies do not cover.

Coverage may cover home health care, assisted living, nursing, adult day care, respite care, and hospice care.

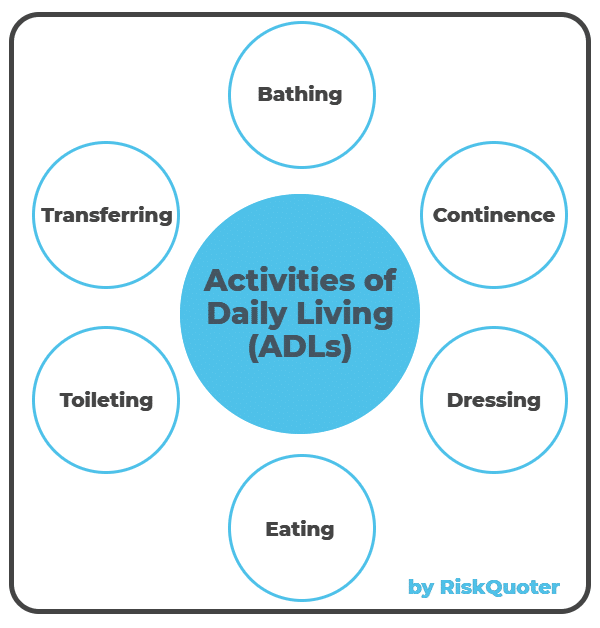

You probably heard about the Six Activities of Daily Living (ADL) used to evaluate your health.

- Bathing

- Continence

- Dressing

- Eating

- Toileting

- Transferring

Additionally, it’s worth noting that you only trigger benefits when you cannot perform at least two out of the six Activities of Daily Living.

Types of Long-Term Care Insurance Policies

There are three types of coverage available.

- Traditional Long-Term Care Insurance

- Hybrid Long Term Care Insurance

- Long-Term Care Insurance Riders

Traditional Long Term Care

Traditional LTC policies serve solely long-term care purposes.

A traditional policy will outline the following:

- Daily Benefit Amount

- The Benefit Period

- Elimination Period

- Inflation Protection

- Included Riders

- Discounts Available

- Underwriting Health Class

While each company’s product varies, you will find the above with all traditional LTC coverage.

The following hybrid policies have primarily replaced the older traditional policies from CNA Long-Term Care Insurance, John Hancock, GE, and Transamerica Long-Term Care Insurance.

As a side note, the CEO of Genworth indicated that their CareScout subsidiary is entering the LTC market.

Hybrid Long Term Care Insurance

A hybrid policy will be a whole life, universal life insurance, or an annuity combined with long-term care benefits.

The appeal of a hybrid policy is that it offers a death benefit or an investment should you never need long-term care. Some prefer this idea vs. paying for a traditional policy that may never be used.

Examples of a hybrid policy are Lincoln National’s Moneyguard Fixed Advantage or Nationwide’s Care Matters II policy.

Long-Term Care Insurance Riders

Several life insurance companies allow the addition of a long-term care rider to universal and whole life insurance policies.

Additionally, some companies offer a basic rider, while others have riders that compare well with a traditional or hybrid policy.

When we discuss your needs, we’ll explain the pros and cons of each type of coverage to you so that you will make an informed decision.

Indemnity vs. Reimbursement: Understanding LTC Payouts

Long-term care insurance policies are either indemnity policies or reimbursement policies.

An indemnity long-term care policy pays the specified benefit of your policy, while a reimbursement policy pays the actual cost of services rendered subject to your policy limits.

Is Long-Term Care Insurance Right for Me? Best Age to Buy LTC

When you’re younger and healthier is the best time to purchase LTC insurance.

Premiums tend to be lower, and you’re more likely to qualify for coverage.

LTC is a good option if you are concerned about needing extended health care someday and what that care would do to your financial situation.

But don’t worry if you wait until later in life to consider coverage, as great options are still available.

How Much Does Long-Term Care Insurance Cost (With Examples)

Long-term care insurance is a good idea if you have the resources to purchase coverage.

And while LTC is expensive, compare that to what could happen to your family and finances if you had to pay for care for 2-3 years.

Long-term care insurance costs vary based on several factors, including age, health status, coverage amount, and specific policy details. Generally, the younger you are when you purchase the insurance, the lower the premiums will likely be.

How much does long-term care insurance cost?

Long-term care policies have many features, riders, etc., available to consider that will affect your pricing.

You can tailor different policies with varying benefit amounts to fit your needs and budget.

Also, remember that additional discounts are available if you apply with your partner.

Sample Pricing

Here are some examples using Lincoln National’s MoneyGuard Fixed Advantage plan.

Just take a look at the guaranteed benefits you receive with this policy.

Age 55 Female – One-time premium = $100,000 – Standard Underwriting, Basic Return of Premium, and 3% compound inflation rate – 4-year benefit duration.

| Policy Year | Age | Monthly LTC Benefit | Total LTC Benefit | Death Benefit | Return of Premium |

|---|---|---|---|---|---|

| 1 | 55 | $5,659 | $284,106 | $152,600 | $70,000 |

| 11 | 65 | $7,605 | $381,815 | $135,818 | $70,000 |

| 21 | 75 | $10,221 | $513,127 | $135,818 | $70,000 |

| 31 | 85 | $13,736 | $689,600 | $135,818 | $70,000 |

| 46 | 100 | $18,461 | $1,074,374 | $135,818 | $70,000 |

Age 55 Male – One-time premium = $100,000 – Standard Underwriting, Basic Return of Premium, and 3% compound inflation rate – 4-year benefit duration.

| Policy Year | Age | Monthly LTC Benefit | Total LTC Benefit | Death Benefit | Return of Premium |

|---|---|---|---|---|---|

| 1 | 55 | $6,078 | $ 305,143 | $145,875 | $70,000 |

| 11 | 65 | $8,169 | $410,087 | $145,875 | $70,000 |

| 21 | 75 | $10,978 | $551,123 | $145,875 | $70,000 |

| 31 | 85 | $14,753 | $740,663 | $145,875 | $70,000 |

| 46 | 100 | $22,985 | $1,153,929 | $145,875 | $70,000 |

How Much Does a Nursing Home Cost?

Long-term care insurance may seem expensive until you consider how much it will cost for your loved one to receive nursing home care, assisted living, adult day care, or in-home services.

Costs vary by the type of services provided and where you live. Here’s a great nursing home cost calculator from AARP to give you an idea of costs.

Here are some examples using the above calculator should you retire to the Sarasota, Florida region.

Average Costs:

| Service | Cost |

|---|---|

| Home Health Aid | $129 Per Hour |

| Adult Day Care 5x Per Week | $2064 Per Month |

| Assisted Living | $4,145 Per Month |

| Semiprivate Nursing Home | $9,490 Per Month |

| Private Nursing Home | $10,615 Per Month |

Statistics show that women tend to need care for longer durations than men, with women averaging 3.7 years of care needed vs. men needing 2.2 years.

Does Medicare Cover Long-Term Care?

Does Medicare cover long-term care?

Medicare will pay for medically necessary skilled long-term care for brief periods of time if the following criteria are met:

- The individual must have had a prior hospital stay of at least three full days.

- The individual must be admitted to the skilled care facility within 30 days of hospital discharge.

- A doctor must certify that skilled care is required.

Medicare limits the days it will pay for long-term care, and care must occur in a skilled nursing facility.

| Number of Days in Skilled Nursing Facility | Coverage |

|---|---|

| Day 1-20 | Medicare Pays 100% of Approved Costs |

| Day 21 – 100 | Patient Pays $204 CoPay Per Day in 2024 |

| Day 101 and Beyond | Medicare Pays Nothing |

Day 21-100 will cost you a minimum of ($204×80) and $16,320 in copays alone!

If you have a Medicare Advantage or Medigap plan, that policy may help with some of the $204 daily copays.

What to Expect from Long-Term Care Insurance Underwriting

Each company has its own set of underwriting guidelines.

All companies have a telephone interview component with a cognitive screening component. Although not often, in some cases, a company may require a face-to-face assessment.

Most companies will review your medical records as part of underwriting. If you don’t visit a physician regularly, underwriting becomes more difficult.

In addition, companies will search prescription databases and the Medical Information Bureau for information.

Certain pre-existing health conditions or disabilities might disqualify individuals from obtaining coverage. Insurers assess applicants’ health and medical history to determine eligibility and pricing.

Top Long-Term Care Insurance Companies in 2024

Many great insurance companies offer long-term care insurance, including:

- Lincoln National – MoneyGuard Fixed Advantage

- Mass Mutual – CareChoice One

- Mutual of Omaha – MutualCare products

- Nationwide – CareMatters II

- OneAmerica – Asset Care

- Pacific Life – PremierCare Choice

- Securian – SecureCare

And with our service, you can see what these companies offer in a no-pressure, no-obligation setting.

Avoid These Long-Term Care Insurance Companies

Which long-term care insurance companies should you avoid?

The good news is that you don’t have to avoid them, as the worst companies put themselves out of business and/or stopped issuing LTC policies.

When financial conditions get so bad for an insurance company, the state where the company is domiciled will order the liquidation of the company.

All states have a Life and Health Insurance Guaranty Association that handles claims and benefits when a company goes under.

Some of the worst companies include:

| Company Name | What Happened? |

|---|---|

| Penn Treaty | Liquidation |

| CNA Long Term Care | Stopped Issuing Policies |

| Genworth | Stopped Issuing Policies |

| John Hancock | Stopped Issuing Policies |

| UNUM | Stopped Issuing Policies |

| Prudential | Stopped Issuing Policies |

Choosing Your LTC Policy

Now that you have decided to purchase long-term care insurance, you must make some important decisions about the policy.

Type of Policy – Will you choose a traditional, hybrid, or rider-based policy?

Benefit Amount – How much coverage do you need daily or monthly? We have guidelines available to help you with this.

Elimination Period – This is the time that must pass before benefits become available. Options include 0, 30, 60, 90, or 180 days before benefits start.

Inflation Protection – You can choose no protection (not recommended), simple inflation, or compounded inflation to keep up with the times.

Policy Features – Each company’s product varies, and you must choose what is most important for your situation.

Policies today offer home-based care as most people want to receive treatment at home.

Discounts – If your spouse/partner needs coverage, discounts are available with some companies.

We’ll help you wade through everything.

Pros of Long-Term Care Insurance

One of the best benefits of LTC is its ability to protect your assets from the high costs of an expensive nursing home stay.

A long-term care policy dictates the management of your healthcare needs.

It may be possible to use 401k assets to purchase LTC protection!

You can set up a 10-pay plan to fund your long-term care.

You may be able to use your HSA to fund insurance premiums.

Always consult your tax advisor to discuss if your qualified long-term care premiums are deductible.

Business owners may benefit from additional business tax deductions.

Cons of Long-Term Care

Cost is the biggest obstacle keeping insureds from buying a long-term care policy.

Choosing the wrong policy is another concern – you must buy one that will address your needs and budget now and far into the future.

If you wait too long, you may not be insurable.

If you previously qualified for a tax deduction but decide to cancel your policy, those prior deductions may become taxable income – As always, consult your tax expert.

Long-Term Care Insurance Tax Deductions: What You Need to Know

As always, you must consult with your tax advisor to get definitive answers to any tax questions, as we do not give tax advice.

If you want the possibility of a tax deduction, make sure your policy is tax-qualified, as most policies issued today are tax-qualified long-term care insurance policies.

Long-Term Care Premium Deductions

Tax-qualified LTC premiums are considered a medical expense as an itemized tax deduction subject to the medical expense limits.

With current rules, medical expenses must exceed 7.5% of your AGI to be deductible. While it’s unlikely to get tax benefits in your younger years, as you can see below, the older age deductions may be substantial, giving you a deduction.

The maximum deductible amount is based on your age. (2024 limits)

| Age | Deductible Limit |

|---|---|

| Age 40 or Less | $470 |

| Age 41 – 50 | $880 |

| Age 51 – 60 | $1760 |

| Age 61 – 70 | $4710 |

| Age 71 + | $5880 |

Self Employed Tax Deduction

If you’re self-employed, you can deduct 100% of the premiums you paid up to the above limits. You don’t have to meet the 7.5% AGI threshold to deduct.

If your business operates as a partnership, LLC, or Subchapter S, the premiums paid on your behalf contribute to your AGI. Yet, you can deduct 100% of the premiums, subject to the above limits. You do not have to meet the 7.5% AGI limits.

C – Corporations can take a 100% business expense deduction and are not subject to the age limits. You should also know that LTC policies are not subject to non-discrimination rules, so you can choose whom to offer coverage.

As always, you must check with your tax advisor about your situation to ensure deductions are available before purchasing coverage.

Taxation of Long-Term Care Benefits

Long-Term Care Benefits Taxation – LTC benefits are generally paid income tax-free under Internal Revenue Code 104(a)(3).

Taxation of Death Benefit – Death benefits are paid to beneficiaries income tax-free under Internal Revenue Code 101 (a)(1).

HSA Accounts and Long Term Care Premiums

If you have a high deductible health plan at work, a Health Savings Account (HSA) allows you to set aside pre-tax money from your wages to pay for qualifying medical expenses.

Long term care insurance premiums are a qualifying medical expense.

If your LTC policy is tax-qualified, premiums can be reimbursed through your HSA, subject to the following limits in 2024.

| Age | Deductible Limit |

|---|---|

| Age 40 or Less | $470 |

| Age 41 – 50 | $880 |

| Age 51 – 60 | $1760 |

| Age 61 – 70 | $4710 |

| Age 71 + | $5880 |

Flexible Spending Accounts and LTC

Your FSA account can not reimburse long-term care premiums.

Long-Term Care Tax Deductions & Partnership Programs by States

Some states offer a credit or tax deduction for premiums you’ve paid for long-term care.

In addition to tax deductions/credits, some states participate in LTC partnership programs that greatly benefit you.

A partnership program typically allows you to exclude some assets from Medicaid spend-down rules equal to the amount of LTC benefit you purchased.

States that participate in partnership programs include:

| State | Partnership Program? |

|---|---|

| Alabama | Yes |

| Alaska | No |

| Arizona | Yes |

| Arkansas | Yes |

| California Long Term Care Insurance | Yes |

| Colorado | Yes |

| Connecticut | Yes |

| Delaware | Yes |

| District of Columbia | No |

| Florida | Yes |

| Georgia | Yes |

| Hawaii | No |

| Idaho | Yes |

| Illinois | Pending |

| Indiana | Yes |

| Iowa | Yes |

| Kansas | Yes |

| Kentucky | Yes |

| Louisiana | Yes |

| Maine | Yes |

| Maryland | Yes |

| Massachusetts | No |

| Michigan | Yes |

| Minnesota | Yes |

| Mississippi | No |

| Missouri | Yes |

| Montana | Yes |

| Nebraska | Yes |

| Nevada | Yes |

| New Hampshire | Yes |

| New Jersey | Yes |

| New Mexico | Yes? |

| New York | Yes |

| North Carolina | Yes |

| North Dakota | Yes |

| Ohio | Yes |

| Oklahoma | Yes |

| Oregon | Yes |

| Pennsylvania | Yes |

| Rhode Island | Yes |

| South Carolina | Yes |

| South Dakota | Yes |

| Tennessee | Yes |

| Texas | Yes |

| Utah | Yes |

| Vermont | Yes |

| Virginia | Yes |

| Washington | Yes |

| West Virginia | Yes |

| Wisconsin | Yes |

| Wyoming | Yes |

Long-Term Care Insurance by State

When considering long-term care insurance, you must review the policies that are available in your home state, as there may be wide variations in products.

Many states (but not all of them) offer Long Term Care Partnership Programs. The benefit to you is that partnership programs allow you to exclude assets from your estate if you have a long-term care insurance policy.

If you have residences in multiple states, it may be possible for you to choose which state to obtain coverage in.

Here are some quick highlights by state:

Arizona Long-Term Care Insurance

When considering long-term care insurance in Arizona, look for policies that qualify under the Long Term Care Partnership Program (most do) as these policies provide additional benefits under the Estate Recovery Program.

California Long-Term Care Insurance

We have a page dedicated to long term care insurance in California.

Connecticut Long-Term Care Insurance

Long-term care insurance in Connecticut that meets the partnership guidelines will provide you with Medicaid asset protection. Additional details may be found here.

Florida Long-Term Care Insurance

You’ll find additional details about long-term care insurance in Florida and how their partnership program works – here.

Maryland Long-Term Care Insurance

Long term care insurance in Maryland that meets the partnership program requirements, offers you additional benefits – Click here for MD details.

New Jersey Long-Term Care Insurance

The long-term care insurance partnership in NJ allows insureds to protect assets equal to the amount of the insurance benefits. You’ll find some basic information here from New Jersey.

Ohio Long-Term Care Insurance

Long-term care insurance in Ohio is also referred to as LTC4ME. Ohio provides additional consumer information at this link.

South Carolina Long-Term Care Insurance

Long-term care insurance policies in South Carolina that are approved partnership policies offer you additional protection. You’ll find additional South Carolina information – here.

Texas Long-Term Care Insurance

A long-term care insurance partnership program is available in Texas, and the insurance department offers consumer information for your review.

Washington State Long-Term Care Insurance

Long-term care insurance in Washington is partnership-approved. Washing has some of the most straightforward and up-to-date information available to consumers.

In addition, Washington started its Wa Cares Fund in 2023, which uses payroll tax deductions to provide up to $36,500 of long-term care benefits.

FAQ

You have questions about long-term care insurance, and we have the answers.

Final Thoughts

Long-term care insurance provides peace of mind for individuals and their families.

Understanding these policies’ coverage, costs, and implications is crucial in making an informed decision about LTC.

And keep in mind that our service is free, with no obligation or pressure to buy. Please request a quote today. Thank you!